piggy bank

I always love articles that are like “X Ways You Can Double Your Savings.”

But then they’re like:

1. Never eat takeout!

2. Send 50% of your paycheck directly to your savings account!

3. Buy all your clothes at Goodwill! Your kids don’t care!

4. Line dry all of your clothes to save money on your electric bill and have Super Fresh Smelling Clothes!

And I’m like:

1. You have clearly never had to run three kids around to practices/events/sports from 2:30 to 7 pm on a Wednesday. Don't you dare judge me. Jerk.

2. And buy food wiiiiith?

3. Have you SEEN what they have at Goodwill?

4. No. Just, no.

I think the folks that write things like this have good intentions. They are probably just trying to be innovative; but instead of being innovative, they are being ridiculous.

Take the whole “Save X% of your paycheck.” It’s never like “Save $5.” Guess what? Most of the time, even the most frugal people can’t save 20% of their paycheck. Because they need that money to live.

I’ve been notoriously lousy at saving money for a few reasons.

1. I like stuff.

2. I have no self-control (which I can partly blame on mental illness but still).

3. See #1

But in the last six months I’ve paid off all of our debt, saved enough money to buy a(nother) house, and really changed the way I feel about myself and my needs overall.*

*Disclaimer: Almost all of my income can go toward debt etc because my husband has a good job.**

**Double disclaimer: Prior to six months ago, I spent every penny of said income. Because I’m that good at being an adult.***

***Not very good at being an adult.

Anyway, here is my list of super practical ways to save money.

They are the things that worked for me; I know they will work for you.

1. Start by itemizing an entire month’s spending.

This is so boring (and also sometimes kind of humiliating), but you have got to start here.

You do not have to use budgeting software or anything fancy. Get a piece of paper and turn it sideways. Make columns for the following: Grocery. Dining out. Mortgage/Rent. Utilities (cable, electricity). Car expenses. Loans/debt. Medical care. Clothing. Gifts. Misc household expenses (like repairs, etc.). We also have a small budget for spending money for both of us and allowance for the big kids.

I took it a step further and made columns for Target and Amazon.

And then I cried.

Once I did this, I was ALARMED by two things:

-

The amount of money I spent at Amazon (mostly on books).

-

The amount of money we spent eating out (seriously it adds up SO fast).

Don’t cry.

I mean, if you are as embarrassed as I was, you probably should just go ahead and get it out.

But then move on. You are here to make changes. You are going to save money. You have to start somewhere. Somewhere is staring your crap spending habits right in the face.

You don’t have to do anything with this list. Unless you want to. I hung it over my desk.

Part 1A (optional for those of you with debt):

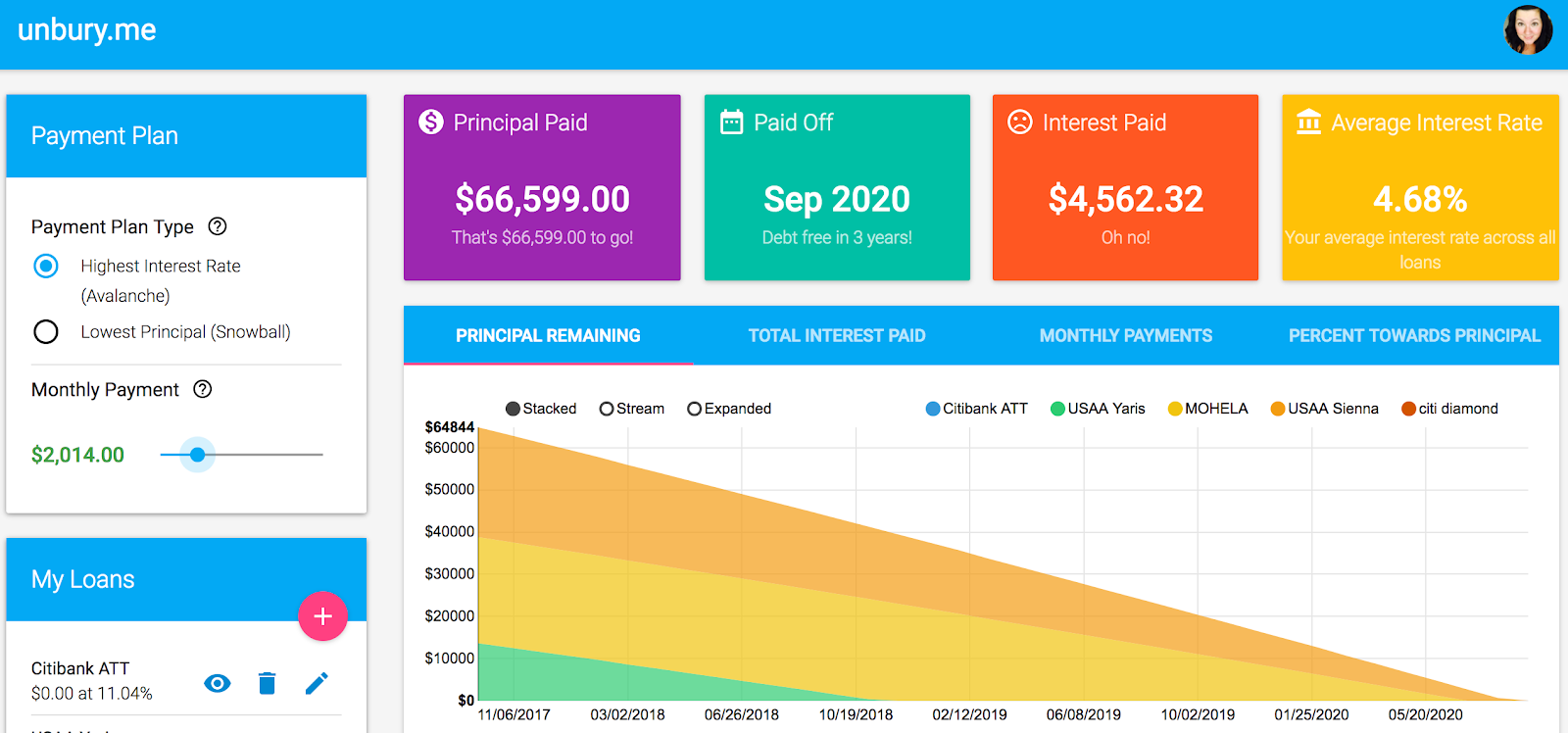

I used unburyme.com to track all of our existing debt. This is free and an awesome way to project various scenarios depending on how much you can pay per month.

We've got two car payments and one student loan left.

This looks infinitely better than it did. I wish I had a screenshot of this screen in March. It was terrifying.

I didn’t like seeing these numbers because it made the debt very real to me. But it was also a very real eye opener.

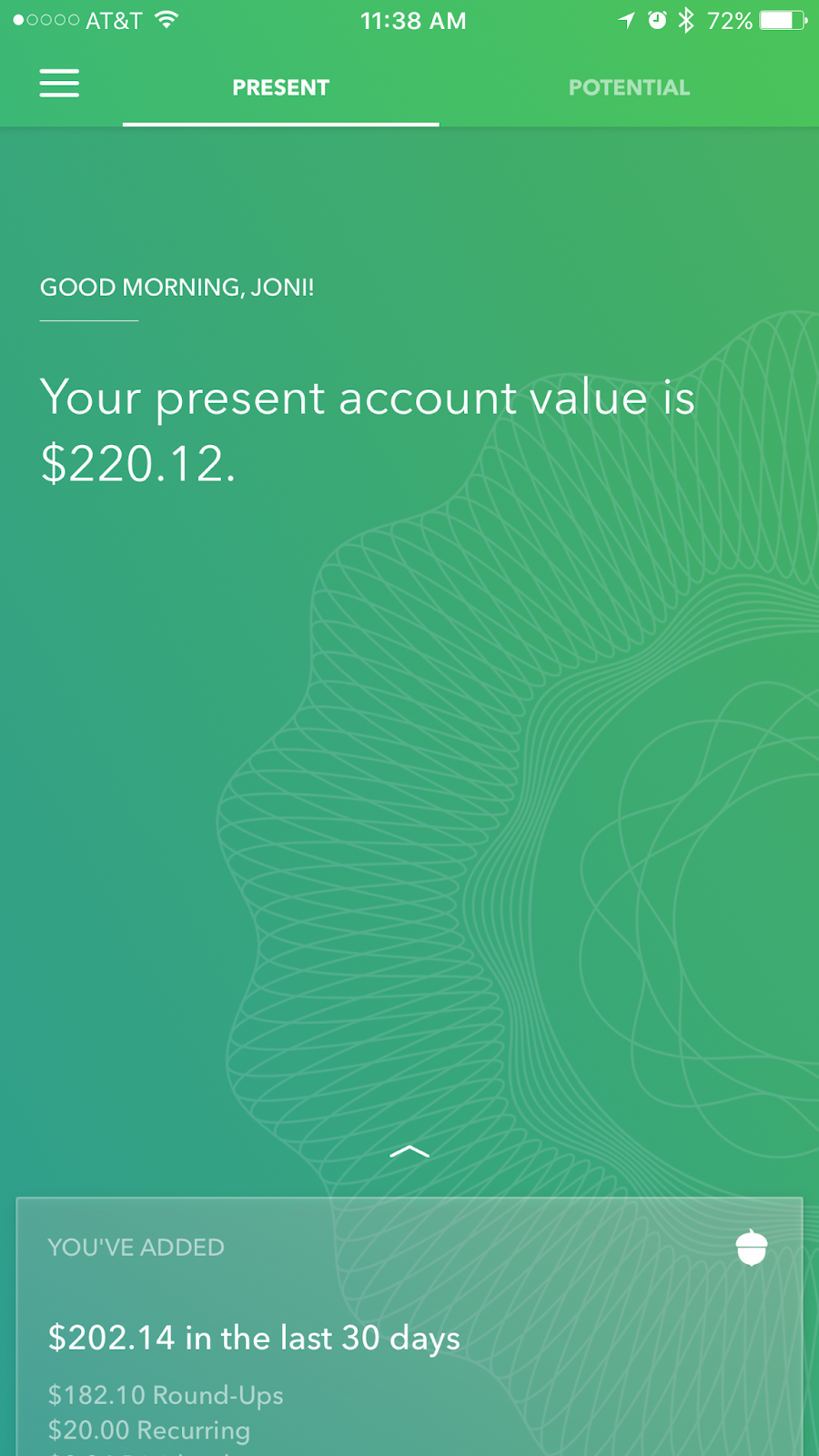

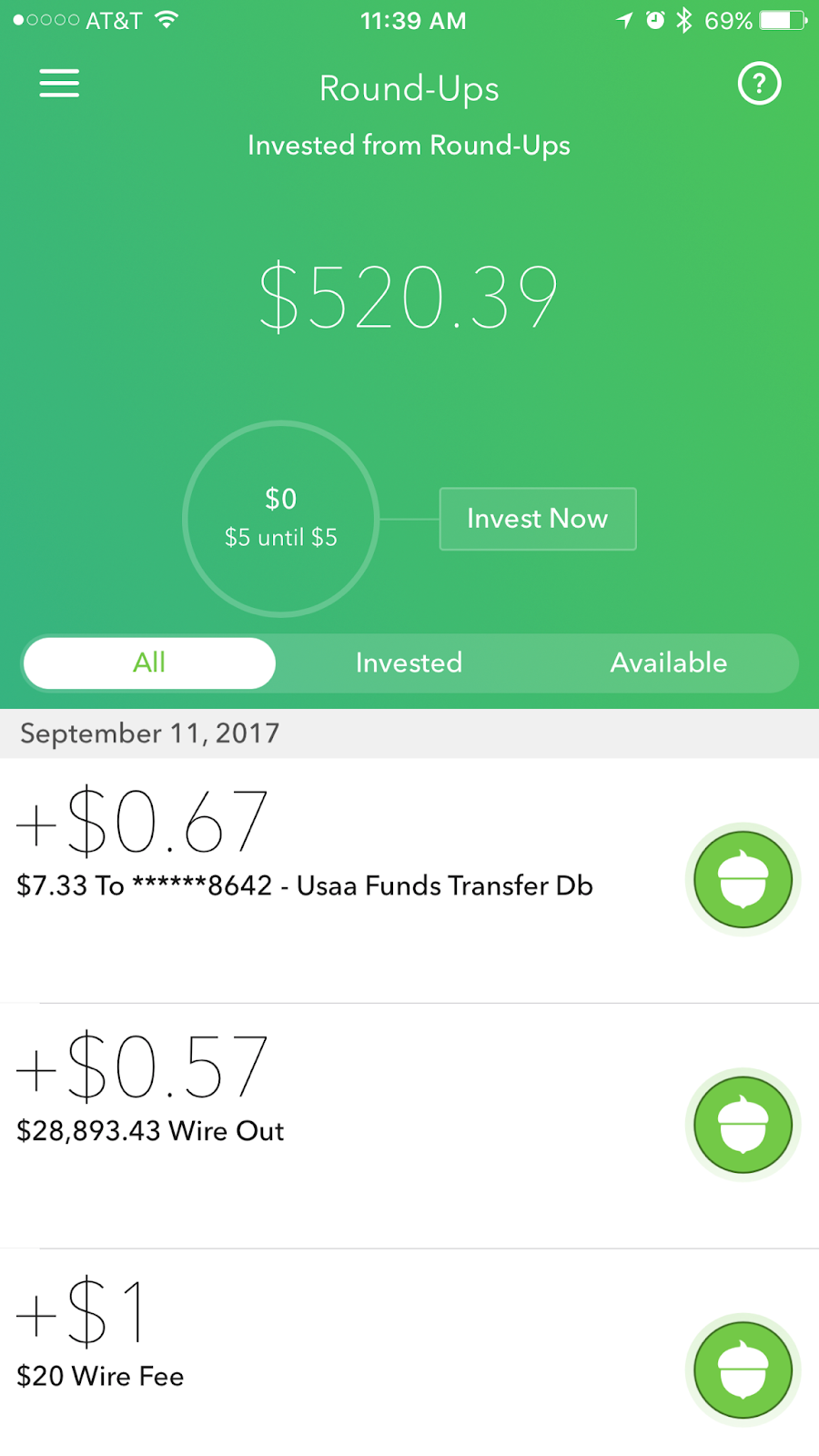

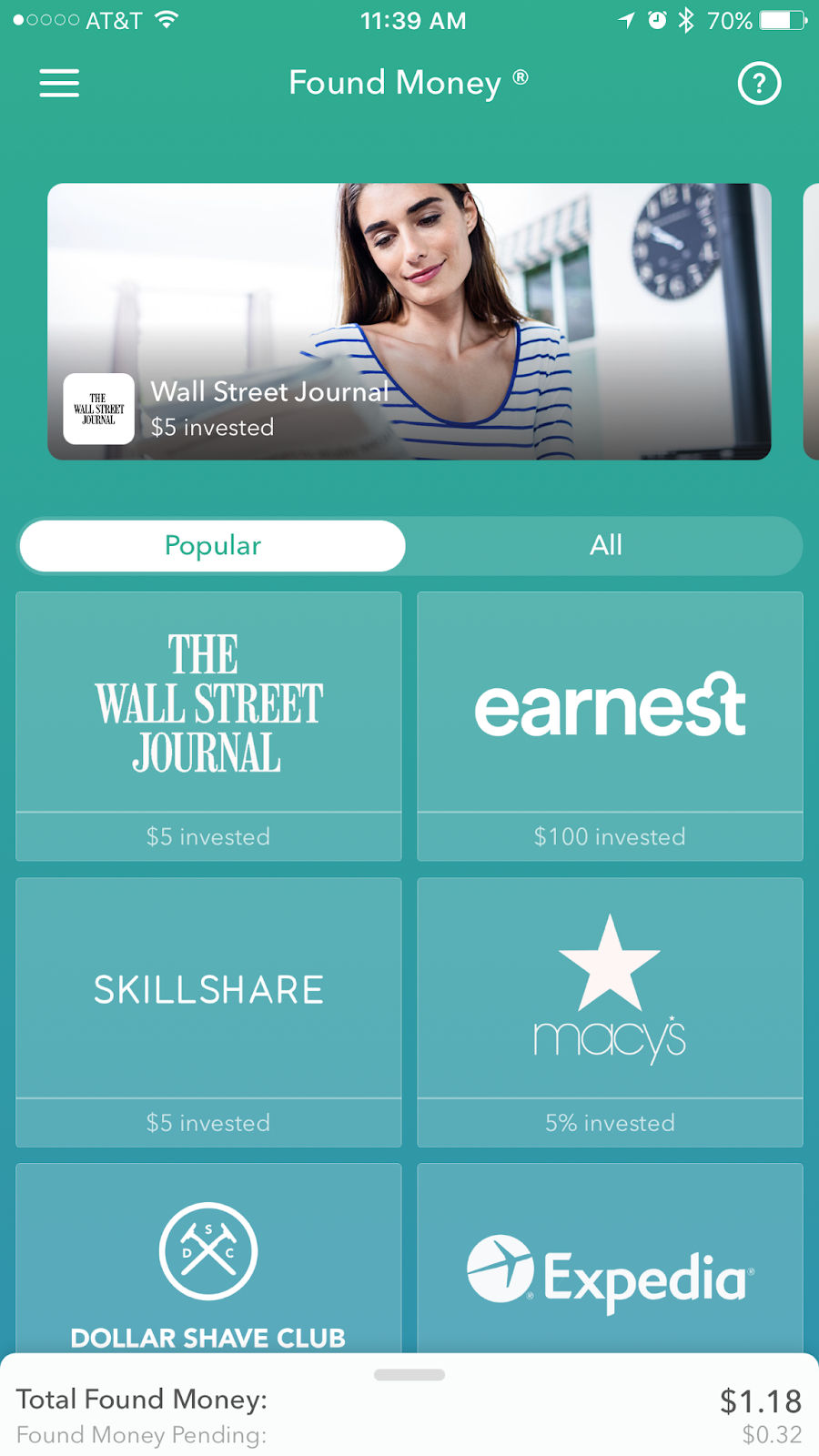

2. Acorns.

This is legitimately one of the most brilliant things ever.

Acorns is a simple investment app.

Don’t be scared of the word investment. You don’t have to know anything to use this. In fact, the very very best way to invest money is to find a place to put it (a good mutual fund, Vanguard is my choice), and forget it is there.

That’s what Acorns does.

You can schedule it to auto-deduct a set amount of money each month (starting at $5). But that’s not the best part. The best part is the Round-Up feature.

Acorns will scan your checking account for any purchases and round them up to the nearest dollar. So you spend $4.25 at Starbucks, Acorns rounds that up to $5 and invests that $.75 automatically.

No crap.

These are actual screenshots from my actual account.

Also, my phone is at 69% battery. LOLZ.

Because it’s an investment, you can’t access that money right away (you have to wait to sell whatever stocks you own), which keeps you from impulse spending. BUT because it’s an investment, you’re earning interest! Which is AWESOME!

I painlessly saved almost $1000 (which I then sold to put toward the down payment on our new house).

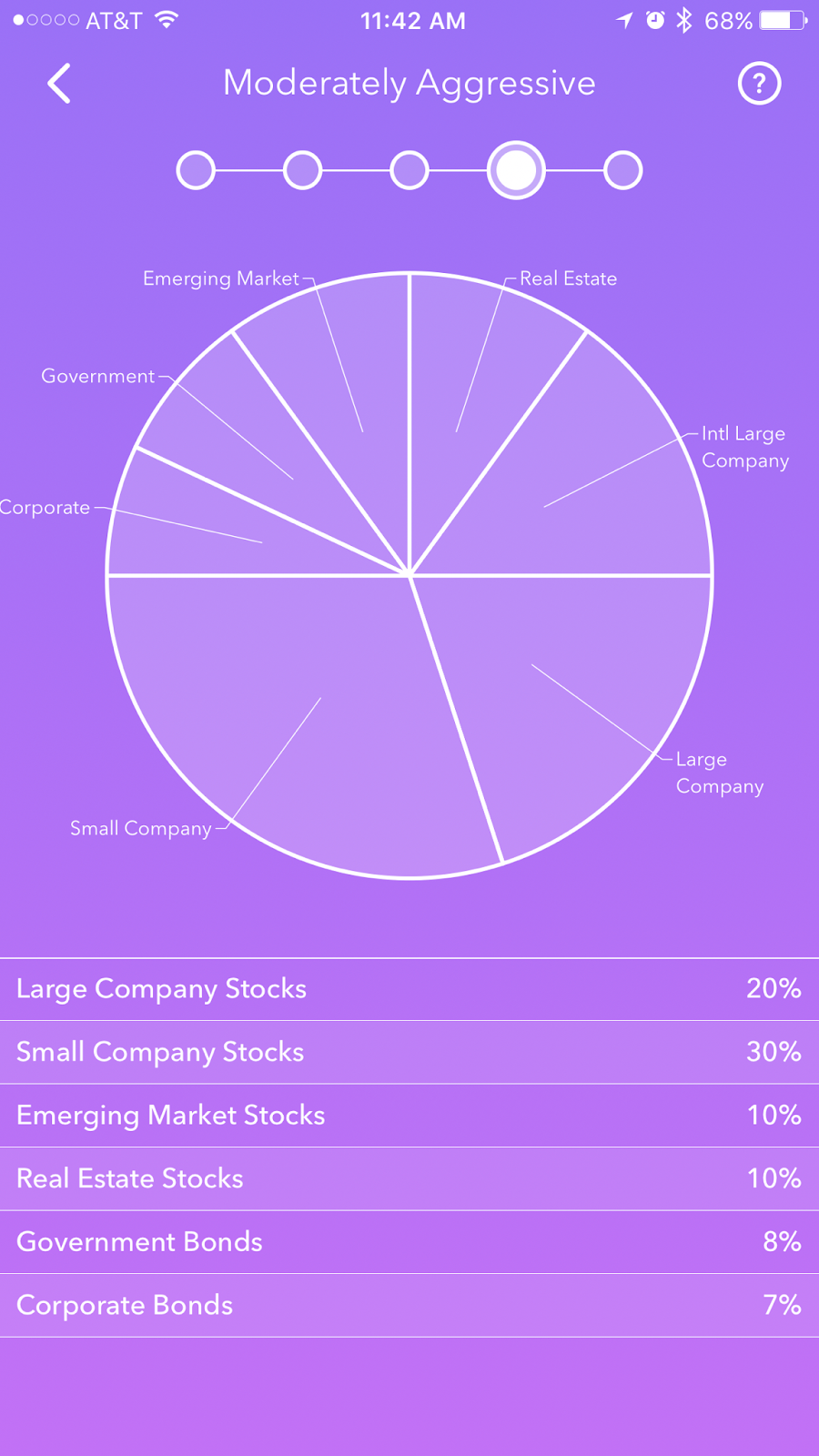

This is how my cash is currently invested:

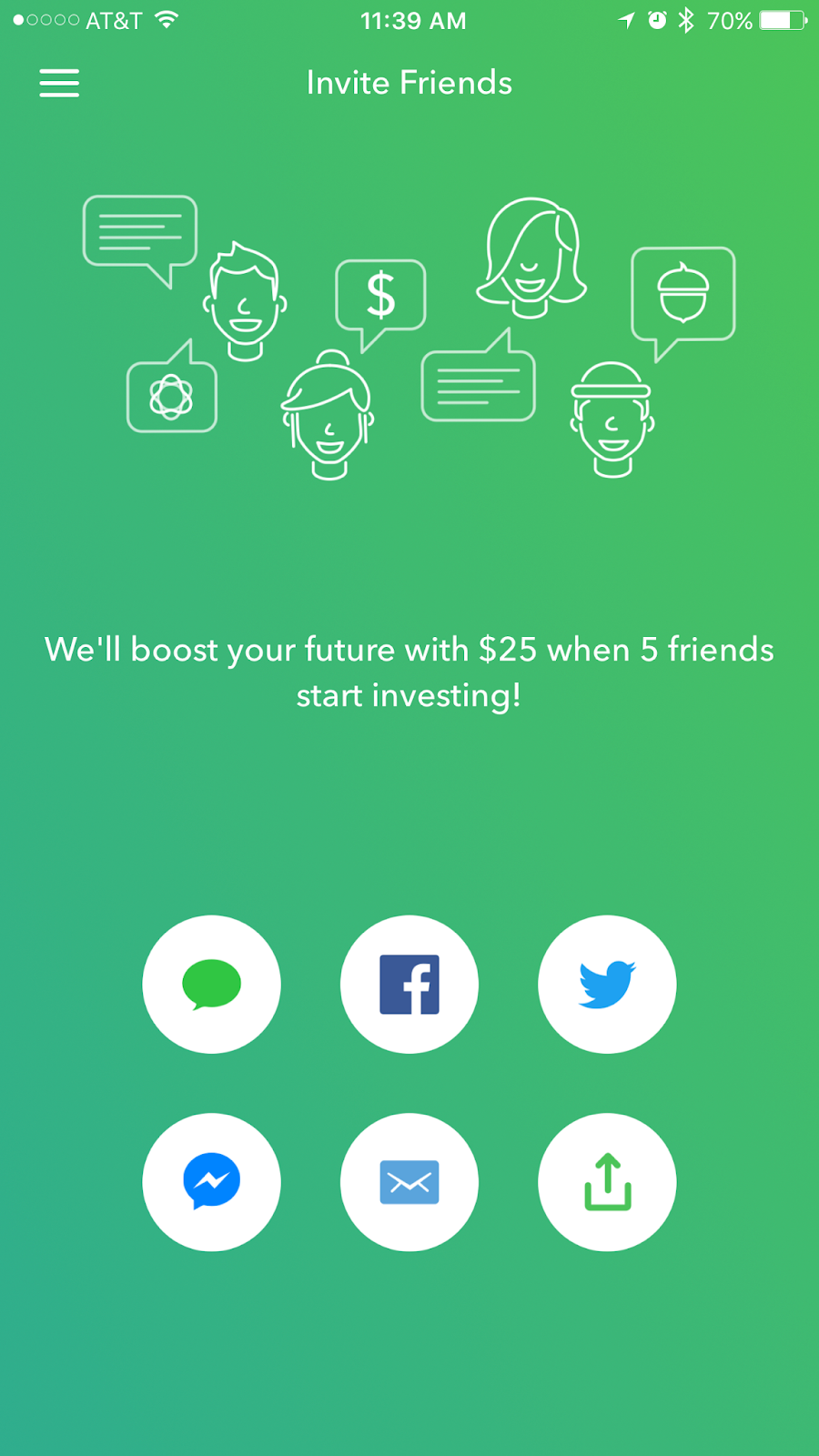

BONUS:

Acorns is partnered with a few businesses (Macy’s and Zappos are two!). Those businesses will invest a small portion of your purchases.

Here’s an account projection with me saving $50 a month plus round-ups.

Bonus bonus:

You can invite your friends and get some cash in your own account!

Seriously, this app is my favorite thing ever.

OK. Next.

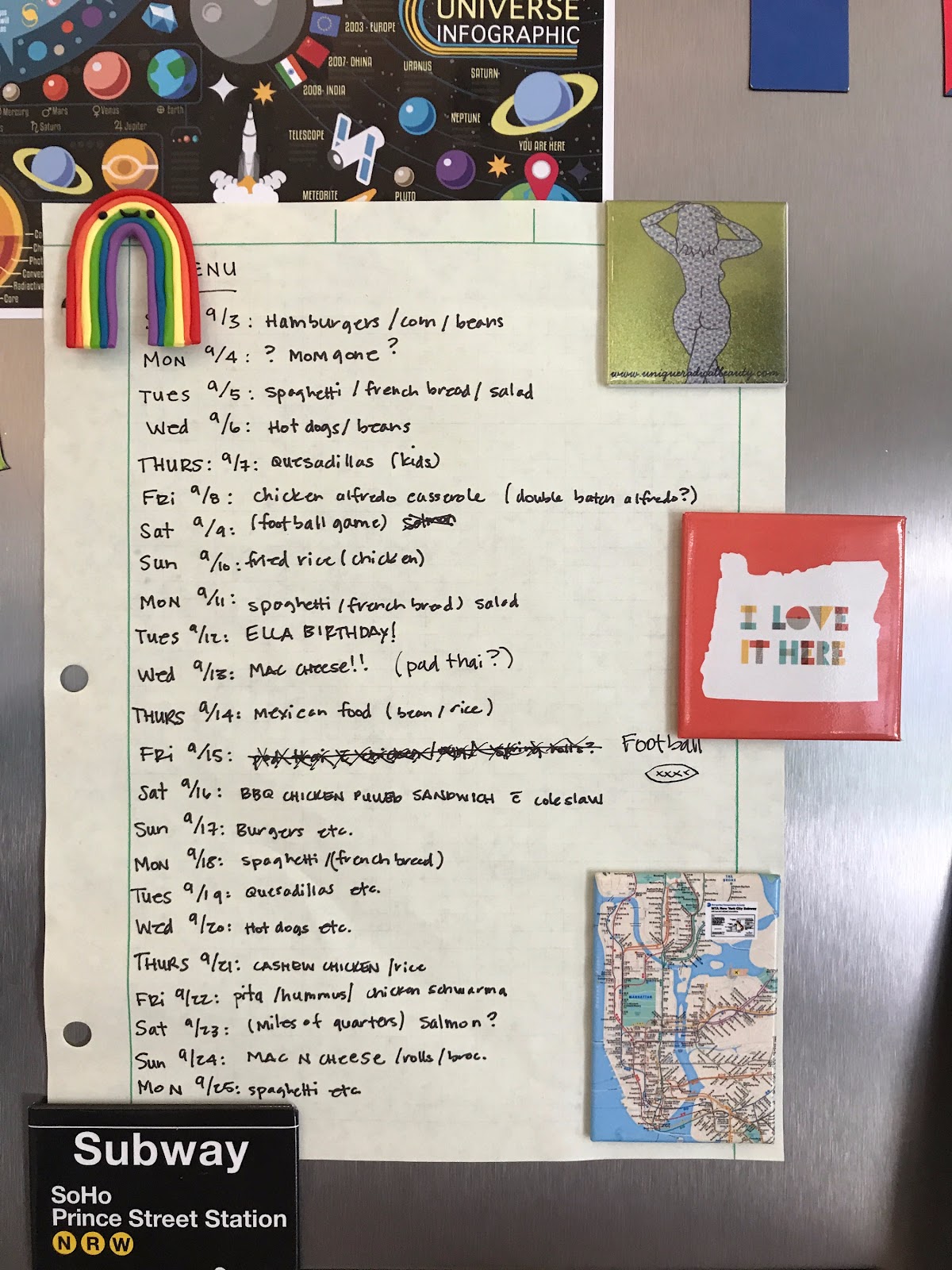

3. Meal plan.

I know, after the Acorns bomb, this is pretty boring. But, it works.

Here is our September menu:

Again, nothing fancy. Pen. Paper.

I make the menu at the beginning of the month. It’s easy because we ALWAYS have spaghetti once a week and we ALWAYS have an easy night (usually hot dogs) when my husband is gone mid-week.

I shop at Costco on Fridays (WITH A LIST) and buy a whole cooked chicken, salmon (every 4 weeks), hamburger (every 2-3 weeks), veggies and fruit, milk and butter, bread, cheese, cereal, and bulk rice and flour (about once every 3 months).

On Sunday I take my more detailed list to the regular old grocery store and buy whatever fill in items I need (sauce things, small produce items like limes or green onions), and anything else I don’t want to buy one thousand of.

This has been the biggest money saver for us, by far. Without a plan, I fall right into “let’s just grab a pizza” mode. Because at 4 or 5 pm, the LAST thing I want to do is think about cooking.

4. Stop shopping on Amazon.

I put this piece of paper over my desk.

Yeah it’s just an A with a line through it. But if I open Amazon on my browser and look up, it’s shaming me into frugality.

I also deleted the Amazon app from my phone. Same-day delivery sucked me in, and you better bet Amazon planned that. Oh $35 of stuff gets it to your door today? But you only need two tubes of Neosporin at $6.99? It’s not hard at all to find $28 worth of stuff you can to your cart.

Do not act like you haven’t done this.

Amazon is a sneaky bastard.

And while you’re at it…

5. Stay out of Target.

You know that Target has craftily devised a way to take all of your money.

I had to go to Target today for birthday candles and powdered sugar.

I spent $246.

To be fair, the things I bought were mostly items for the new house, but I definitely did not need $10 face wash and $12 lotion.

Case in point: AVOID.

6. Set your checking to auto-save.

Not 50% of your paycheck. Let's be real.

Start with something manageable, $5, $10, $50, and have it just auto-transfer. My checking account (with USAA) has a feature similar to Acorns. It will round-up to the nearest dollar and put that in savings for me. It's a lot easier to save money you never see.

To keep myself from being tempted to touch that money, I have the account hidden on my banking app.

7. Make a goal.

This is less about saving money and more about motivation.

Our goal was two-fold: 1. Pay off debt so we can eventually retire. 2. Buy new house closer to husband's work so he doesn't have to be gone three days a week.

With those two possibilities on the horizon, it was a lot easier to say no to pizza.

I never thought I'd be the kind of person who would have enough money in savings to cover any emergency, much less know about investments (like what even IS the stock market?). But I became that person, and I like her a lot.

You got this.